Western Europe Photo Printing Sector Returns to Value Growth

Western European Photo output value is rising, driven for the first time in many years by all three Photo categories (Photo Prints, Photobooks and Photo-Merchandise). The market was up 3% in 2019.

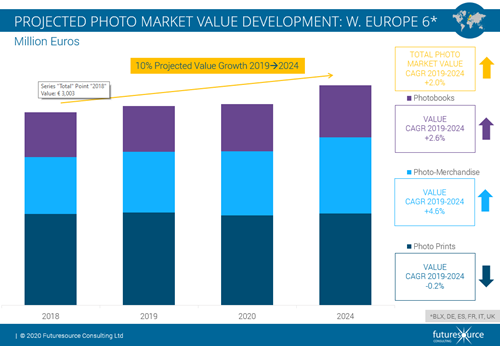

Futuresource's latest (July 2020) photo output reports, covering the top-6 markets in Western Europe (Benelux, France, Germany, Italy, Spain and the UK, which account for 75%+ of total Western European Photo market value) details the progress of this sector in recent years and provide an outlook to 2024.

The continuing popularity of photo prints with the millennials and gen-z, and the success of some more recent app-based resellers, contributed to a 1.3% rise in photo prints value in 2019 (a pivot from declines over many years up to 2019), which was coupled with photobooks and photo-merchandise returning 1.8% and 7.4% value growth respectively.

COVID-19 lockdowns in H1 2020 and retail closures during this period impacted on retail (on-site) photo orders. Some customers moved online instead, leading to fears amongst retailers that they will not recover all of this business. A significant shake-out in the retail minilab installed base in the last 18 months has also contributed to the continuing on-site photo printing decline, although the (retail) instant print photo kiosk sector remains buoyant in many Western European markets.

There was some significant uplift in photobook and some photo-merchandise orders in March, April and May 2020, driven by consumers at home with time on their hands. (Indeed, some resellers reported acquisition of new customers by up to 30% during H1 2020). Resellers, however, saw some slowdown in June and July, as lockdowns eased.

As a result of the impact of retail closures during H1 2020, photo prints value is set to fall by 3% in 2020, before continuing the growth experienced in 2019 over the next few years. Volumes are still declining overall, but younger customers in particular are more agnostic to price and the instant print photo kiosk and web-to-home channels are still exhibiting volume growth.

Photobooks is coming a bifurcated sector, with larger, lay-flat books with high quality digital paper and printing, or printed on silver halide photo paper, often with a rising average number of pages for repeat customers driving value at the top-end, whilst “ready to use” (targeting social media) or “quick to create”, app-based photobooks are gaining volume traction at the lower-cost end of the market. The overall 2020 outloo for photobooks is an 8% volume rise, although price competition during H1 2020 and into H2 is set to push the ASP down in 2020 (and restrict value growth to ~3%).

Photo-merchandise volume is expected to rise by 10% in 2020, riding on the H1 "lockdown" spike, but price competition will deliver a lower, 6% value rise (relatively in line with 2019). Photo cards (and general web to print greetings cards) took a huge upswing in H1 2020. This was felt especially in the UK, Benelux region and Germany, where greetings cards are the most popular, as consumers were not able to purchase cards from retailers. There are hopes that some of these new customers will become permanent e-commerce customers for web to print cards (including photo cards) and for non-photo gifting.

For several years now, the millennials, and, latterly, gen-z have shown an interest in photo prints, having grown up in an era of digital imaging. This has partially been driven by the success of overall, and particular popularity with these demographics of instant print cameras, (e.g.: Fujifilm, Polaroid), which then sometimes lead these consumers to instant print photo kiosk printing in-store, or web to home orders, as they seek a higher quality image. It is not uncommon for several photo prints to be used as wall décor and changed regularly. These demographics are generally not volume customers, and are therefore relatively agnostic to high instant print photo kiosk prices (2020 ASP €0.39 per print) or ordering a set of retro or square photo prints from a website or app, which carry a much higher price than the 10x15cm online photo print average price of around €0.14 (2020) across the Western Europe-6 region.

The rise of the ‘fleet of foot’ photo app is still on the radar of the wider photo industry with Cheerz, Free Prints, Free Prints Photobooks, LaLaLab, Popsa and ReSnap all examples of this. Indeed, some of these more recent app-based resellers have been subsumed into existing photo brands or print service providers (e.g.: Albelli, CeWe, Photoweb). However, the cost to optimise for apps and HTML-5 web orders across iOS & Android, coupled with a website offering is not always palatable to larger players, which offer a much deeper range of SKUs. There is also a concern that many consumers do not want to have apps that they only use occasionally "cluttering up" their Smartphones.

About the author

Jeremy joined Futuresource Consulting in 2001. He holds a degree in French from Kings College, University of London. Jeremy is a member of the Professional AV team. He focuses on Signal Distribution, Meeting Room Control, AV Managed Services, Interactive Displays, Professional Lighting and Esports.

In previous Futuresource roles, Jeremy was part of the Imaging team covering consumer camera and photo output markets and, prior to this, a member of the Home Entertainment team, tracking the global pre-recorded media manufacturing and storage media sectors. Jeremy has managed two research and analysis teams during his years with Futuresource, as well a wide variety of syndicated and custom research projects.

Latest Print & Imaging Posts